AllianceBernstein Large Cap Growth Strategy

MARKET OVERVIEW

Equities gained in June, capping another solid quarter. The S&P 500 gained 3.58% for the month and 4.28% for the quarter as strong performance among several Magnificent Seven (Mag 7) constituents carried index returns. Growth stocks outperformed value stocks for the quarter, with the Russell 1000 Growth Index increasing 8.33% while the Russell 1000 Value Index decreased 2.16%. Technology, communication services and utilities led outperformance within the Russell 1000 Growth for the quarter, while materials, industrials and financials lagged the most on a relative basis.

Domestic equity indices continued this year’s rally in 2Q:24, leaving the Russell 1000 Growth up 20.70% year to date (YTD) as of the time of this writing. Sector and individual stock performance remains highly concentrated as NVIDIA, Apple and Alphabet Inc. each appreciated over 20% for the quarter while Microsoft, Meta Platforms and Amazon saw increases in the low to mid- single digits. We welcome the relatively uncorrelated Mag 7 performances but are increasingly wary of the concentrated performance. For the first half of the year, the Mag 7 drove two-thirds of the S&P 500 gains. For the most recent quarter, S&P 500 earnings grew 5.8% year over year; excluding the Mag 7, the S&P 500’s earnings declined 1.8%. Quarterly performance dispersion between the S&P 500 (up 4.3%) and the equal-weighted version of the S&P 500 (down 2.7%) has defied calls for a broadening of market leadership down the capitalization spectrum. Second-quarter earnings and back-half outlooks will determine any meaningful inflection.

The US Large Cap Growth Portfolio rose in absolute terms but underperformed the Russell 1000 Growth benchmark during the quarter and for the year to date, gross and net of fees. Not holding Apple and Tesla detracted from relative returns during the quarter after providing a significant tailwind in 1Q:24. Apple’s performance was largely driven by hopes that artificial intelligence (AI) integration into new iPhone versions will drive consumers to upgrade phones sooner since Apple Intelligence will be available on only the newest iPhone models. It remains to be seen whether features like a smarter Siri can compress the upgrade cycle and drive sustainably higher upgrade volume. Having a new upgrade feature outside an improved camera or battery life will spark interest from early adopters but an immediate broad adoption is not a given since AI features will likely be feathered in over time. While not an exact comparison, we note that adoption of Microsoft Copilot remains underwhelming. Infrastructure build to support AI training has been parabolic over the last year, but commercialization success has not yet catalyzed revenue outside of accelerating migration of workloads to the cloud. We are scrutinizing every one of the Mag 7’s embrace of AI to distinguish between hope and likely impact. We continue to assess Apple’s reinvestment efforts, considering the AI opportunity. Tesla’s troubles of increased competition and slowing electric vehicle demand remain intact, making the stock’s move higher most likely mean reversion and/or a relief rally now that CEO Elon Musk’s compensation vote is over.

Russell 1000 Growth sector performance YTD repeats what we saw in 2023—communication services and technology continue to dominate performance. Despite appreciating over 15% YTD, the healthcare sector lags the index by roughly 5%. We expect continued strength from the healthcare sector as post-COVID-19 normalization allows for the typically steady demand to shine through. We expect volatility as we approach the November election but place very low odds of meaningful regulatory reform. Gridlock in Washington, DC, tends to favor the status quo. Idiosyncratic opportunities ranging from AI adoption to growth of highly profitable core businesses, like Vertex Pharmaceuticals’ cystic fibrosis franchise, continue to drive our optimism. As valuations continue to stretch for some AI winners, pressure increases for investment dollars to flow toward more attractively priced opportunities. We view healthcare as positioned well to benefit.

Vertex Pharmaceuticals: Continued Core Cystic Fibrosis Strength, Pipeline Executing

Vertex contributed to relative performance during the quarter on solid 1Q:24 earnings results that beat on top and bottom lines, in addition to positive data from the company’s drug pipeline. Vertex is best known for its cystic fibrosis (CF) therapies that improve life expectancy for CF patients, with long patent protection and few competitors. We expect Vertex’s CF business to continue to grow, AB Large Cap Growth Fund Advisor Class: APGYX Quarterly Commentary 2 supported by rising penetration of existing therapies and new product development. Additional upside opportunities for growth can be found in the company’s development pipeline, including a recently approved gene-editing drug for beta thalassemia and sickle cell disease, as well as ongoing clinical trials for non-opioid pain relief, Type 1 diabetes and kidney disease. We believe Vertex’s strong internal research and development (R&D) engine and efficient balance sheet should support above-industry-average profitability over the long term.

Veeva Systems: Reduced Guidance on Soft Spending Environment, Long-Term Opportunity Intact

Veeva Systems, the leading provider of software solutions for the life-sciences industry, detracted from relative performance during the quarter after cutting full-year sales guidance despite posting total sales that grew more than 20% year over year. The company’s reduction in guidance was driven by customer delays of project timing and slower spending in the small and midsize business segment due to ongoing macroeconomic challenges. Veeva’s customers pointed to slowed spending on certain IT products as AI tool spending was prioritized higher, a trend we’ve seen across software companies this year. We continue to have a positive view of Veeva’s competitive position and growth opportunity but acknowledge the near-term headwinds the company faces. Long term, Veeva retains a pathway for growth from its R&D solutions business that offers a unified platform for clinical, regulatory, quality and safety functions—an industry first, as unassociated end-point solutions are the current norm. The top five (held) contributors to relative performance during the second quarter were Arista Networks, QUALCOMM, Costco Wholesale, Vertex Pharmaceuticals and Intuitive Surgical.

The top five (held) detractors from relative performance during the second quarter were Monster Beverage, Veeva Systems, Visa, Copart and Idexx Laboratories.

As always, thank you for your continued support.

— John Fogarty and Vinay Thapar

DISCLOSURES

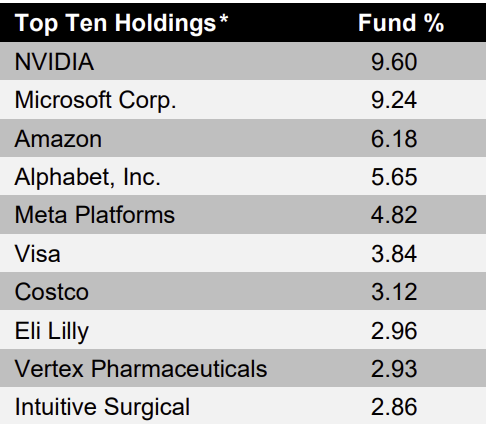

*Based on a representative account as of 06/30/24. Holdings, characteristics and weightings (which are equity-only weightings and exclude cash) will vary over time. They are provided for informational purposes only and should not be deemed as a recommendation to buy or sell the securities mentioned.

A WORD ABOUT RISK Market Risk: The market values of the Portfolio’s holdings rise and fall from day to day, so investments may lose value. Focused Portfolio Risk: Portfolios that hold a smaller number of securities may be more volatile than more diversified portfolios, since gains or losses from each security will have a greater impact on the portfolio’s overall value. Foreign (Non-US) Risk: Non-US securities may be more volatile because of political, regulatory, market and economic uncertainties associated with such securities. Fluctuations in currency exchange rates may negatively affect the value of the investment or reduce returns. These risks are magnified in emerging or developing markets. Derivatives Risk: Investing in derivative instruments such as options, futures, forwards or swaps can be riskier than traditional investments, and may be more volatile, especially in a down market. References to specific securities are provided solely in the context of the analysis presented and are not to be considered recommendations by AllianceBernstein. AllianceBernstein and its affiliates may have positions in, and may effect transactions in, the markets, industry sectors and companies described herein. Investors should consider the investment objectives, risks, charges and expenses of the Fund/Portfolio carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, contact your AB representative. Please read the prospectus and/or summary prospectus carefully before investing. Investment Products Offered: Are Not FDIC Insured | May Lose Value | Are Not Bank Guaranteed The Russell 1000 Growth Index represents the performance of large-cap growth companies within the US. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein fund. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the Adviser of the funds. The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein ® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

CONFIDENTIALITY NOTICE: This email may contain privileged or confidential information and is for the sole use of the intended recipient(s). Any unauthorized use or disclosure of this communication is prohibited. If you believe that you have received this email in error, please notify the sender immediately and delete it from your system.

NO OFFER OR SOLICITATION: The contents of this electronic mail message: (i) do not constitute an offer of securities or a solicitation of an offer to buy securities, and (ii) may not be relied upon in making an investment decision related to any investment offering Axxcess Wealth Management, LLC, an SEC Registered Investment Advisor. Axxcess does not warrant the accuracy or completeness of the information contained herein. Opinions are our current opinions and are subject to change without notice. Prices, quotes, rates are subject to change without notice. Generally, investments are NOT FDIC INSURED, NOT BANK GUARANTEED and MAY LOSE VALUE.

This message may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

AWM often communicates with its clients and prospective clients through electronic mail (“email”), short message service (“SMS”), and other electronic means. Your privacy and security are very important to us. AWM makes every effort to ensure that electronic communications do not contain sensitive information. We remind our clients and others not to send AWM private information over email. If you have sensitive data to deliver, we can provide secure means for such delivery.

Please note: AWM does not accept trading or money movement instructions via email.

All emails and business-related SMS communications are sent through systems that can be archived and monitored. Please contact us at www.axxcesswealth.com for our approved texting number. As a registered investment advisor, AWM emails and SMS communications may be subject to inspection by the Chief Compliance Officer (“CCO”) of AWM or the securities regulators.

If you have received an email from AWM in error, we ask that you contact the sender and destroy the email and its contents.

If you have any questions regarding our email policies, please Contact Us.